I went to see a movie recently with my family (I did fall asleep but that is neither here nor there) Hugh Jackman as a shepherd who reads detective novels to his sheep every night. He dies. The sheep are on the case to get to the bottom of it, turns out they learned a thing or two from Hugh. For those of you who are into sheep movies or the rugged and handsome Hugh Jackman I would recommend it. Well, I can recommend the first 20 and last 15 minutes of it. Great show.

Consider me Hugh Jackman, reading you a story you may not have realized was being told.

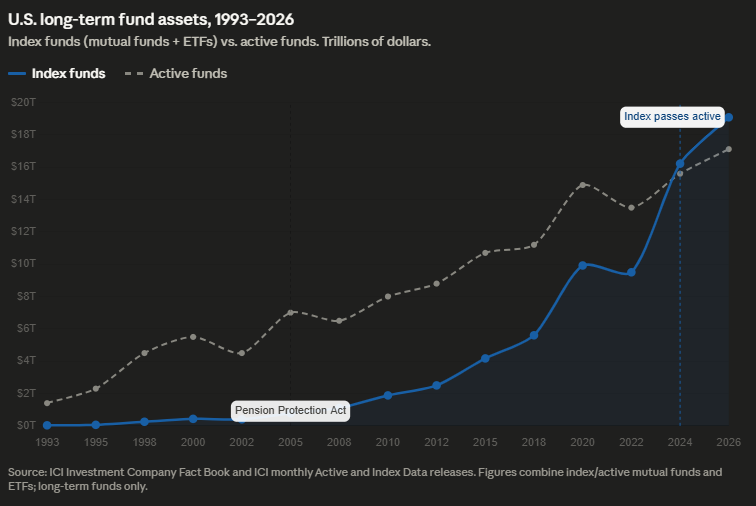

Index funds have been a great financial innovation. They drove costs down. They gave ordinary investors broad market exposure for almost nothing. More importantly, they forced active managers to bring their fees down too. Expense ratios that used to run 1.5 percent now run closer to 0.5 percent. Index funds didn’t cause all of that, but they caused a lot of it. Every investor benefits, whether they own an index fund or not.

What concerns me isn’t the index fund. It’s the amount of money flowing in without anyone deciding to put it there. Fifteen years ago the flows into index funds were a fraction of what they are today, and what flowed in was spread more evenly across the market. Today it piles into the same seven names. In my opinion, index funds are on their way to being victims of their own success.

How a single law from 2006 rewired everything

Most of this traces back to a piece of legislation almost nobody remembers: the Pension Protection Act of 2006.

Before 2006, signing up for your company’s 401(k) was opt-in. You had to fill out forms. About 60 percent of eligible workers participated. After 2006, the default flipped. Now you have to fill out paperwork to not participate and who wants to do that? Another login? Nah, index funds for me it is. Participation rates jumped past 90 percent at plans that adopted the new defaults.

The same law created something with the unpoetic name of “Qualified Default Investment Alternative.” Bureaucratic shorthand for “where we put your money if you don’t tell us where to put it.” That default became the target-date fund. The SECURE Act of 2019 and SECURE 2.0 in 2022 made automatic enrollment basically mandatory for new plans.

Today, target-date funds hold $4.8 trillion, up 21 percent in just the last year. Vanguard alone runs $1.79 trillion of that. And target-date funds, almost without exception, invest by buying broad index funds in proportion to company size.

So here is what happens every two weeks at scale. Payroll runs. Money flows automatically into target-date funds. The target-date funds buy index funds. The index funds buy more of the biggest companies. Nobody decides anything. The system is on autopilot. And it gets bigger every pay period.

Start with the number that surprises most people. The S&P 500 has 503 stocks. But corrected for how concentrated the holdings are, it is mathematically equivalent to owning 54. The seven biggest companies (Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta, Tesla) make up about 30 percent of the index. The top ten are 35 percent. When you tell yourself you have “diversified” by owning an S&P 500 fund, you have bet a third of your money on seven companies.

On May 20, 2026, Nvidia raised its quarterly dividend by 2,400 percent (one cent per share to twenty-five) and authorized $80 billion in new buybacks. The dividend yield of the entire S&P 500 moved from 1.07 percent to 1.10 percent on Nvidia’s decision alone. One company moved the yield of 500 stocks. That is not how diversification is supposed to work.

While you are reading this, the system is also changing its own rules. Two of the largest IPOs in history are about to hit the market. SpaceX is reportedly targeting a Nasdaq listing on June 12, 2026, at a target valuation of $1.75 trillion based on its public S-1 filing. OpenAI has signaled plans to file later this year at a reported target above $1 trillion, according to reporting in the Wall Street Journal and Reuters. Final terms for both have not been confirmed at the time of this writing. Under existing S&P 500 rules, neither would qualify for inclusion. They fail the twelve-month seasoning requirement and the profitability test. So, on April 30, 2026, S&P Dow Jones Indices opened a formal consultation on rule changes that, by their timing alone, appear designed to accommodate them. Imagine that. Neither of these companies would qualify based on historic methodology (which seems quite sound to me) but now they change the rules? Rules exist for a reason, yes over time rules can and do change, but not like this, and not to this magnitude. At least the rules they’re changing aren’t going to impact millions of Americans’ hard-earned dollars. Oh wait… The consultation closes May 28. Proposed implementation: June 8. Three days before SpaceX is expected to price.

I suspect something else might also be contributing to the rule changes. How on earth would the market absorb so much stock without using passive money to do it? You need the money of those that aren’t paying attention to help get this done.

When Tesla joined the S&P 500 in December 2020, index funds had to buy roughly $80 billion of its stock in a single rebalancing. To fund that, the same funds sold $80 billion of the other 499 companies proportionally. The buying alone pushed the stock up 70 percent between announcement and inclusion. Passive money tracking the S&P 500 has grown from $5-6 trillion in 2020 to roughly $9 trillion today. SpaceX at $1.75 trillion would enter at three to four times Tesla’s weight. The forced buying could approach $200 to $350 billion. OpenAI would add roughly another $130 billion. The forced selling of existing index members to fund those purchases would be proportional. This is the largest absorption in the index’s history. The rules are being rewritten to allow it.

The textbook view of markets is that smart money keeps the market efficient. If a stock gets too expensive, hedge funds short it. That used to be more true than it is now. Research published in 2020 showed that for every $1 flowing into the market, about $5 of market cap gets created. For the biggest stocks, the multiplier runs to $75 or $100 of market cap per dollar of inflow. The market hasn’t stopped pricing stocks entirely. It just absorbs flows now.

Remember Beanie Babies? In the late 1990s, people lining up at Hallmark Stores elbows flying to try and get a peace bear (ironically). Not because the toys were worth hundreds of dollars. Because everyone assumed someone else would pay more. The price wasn’t the price. The price was the bid.

My heart goes out to those poor Hallmark employees in the late 90’s who were thrown into Beanie Baby crowd control against their will. Also, if you want to prove my theory wrong, I have a Princess Diana Bear I will sell you for $100,000. She is in beautiful condition & ready to be displayed.

A cap-weighted index fund operates on the same principle. It doesn’t ask whether Apple or Nvidia are priced correctly. It buys what’s biggest, in proportion to how big it is. The bid moves the price. The price draws more bid. Repeat for twenty years.

This has broken before

The idea that “automatic, price-blind buying at scale can distort the market until something gives” is not theoretical. It has happened twice in the last forty years. Each is worth a quick look.

Portfolio insurance, 1987. In the early 1980s, two finance professors created a product that promised institutional investors all the upside of stocks with limited downside. The trick was a mathematical rule: as the market falls, sell stock futures automatically; as it rises, buy them back. It was clean, scientific, and it worked. By October 1987, between $60 and $100 billion was being managed this way.

On October 19, 1987 (Black Monday), the system worked exactly as designed and destroyed itself doing it. As stocks fell, the models told everyone to sell. The selling pushed prices down further. That triggered more selling. The Dow dropped 22.6 percent in a single session, still the largest one-day decline in American market history. Wells Fargo alone sold $1.6 billion in stock futures that day. Time magazine, in its post-crash coverage (“The Culprits Behind the Crash?”), summed it up in seven words: “the scheme was undone by its own success.”

What we have today works on the same principle: automatic, price-blind buying at scale. The only difference is that it has been running for twenty years on the way up instead of one day on the way down.

XIV, 2018. In 2010, Credit Suisse launched a product called XIV that let you bet against market volatility. Essentially a bet that things would stay calm. It worked spectacularly, returning over 1,000 percent through early 2018. The product had a mechanical rule: when volatility rose, it had to buy more volatility futures to maintain its target position. On February 5, 2018, volatility spiked 115 percent in a single day. XIV’s mechanical buying pushed volatility futures even higher, which forced more buying, which pushed them higher still. The product lost 97 percent in one afternoon. Credit Suisse shut it down within the week.

The lesson of XIV is the part that should make any index fund holder uncomfortable. At sufficient scale, the act of buying moves the very thing the buyer thinks they are tracking. The mechanism stops responding to the market and starts being the market.

Two new layers have plugged into the same machine.

The first is AI. As of March 2026, 62 percent of American retail investors are using AI tools to inform investment decisions. More than half use ChatGPT. Among Gen Z, the figure is 68 percent. When you ask any major AI model how to invest, the answer is essentially identical across models. Low-cost broad-market index funds. Dollar-cost average. Long horizon. Don’t pick stocks. This isn’t because the AI is independently reasoning. The AI was trained on decades of internet financial writing that has converged on one answer. Ten million people asking ChatGPT do not get ten million answers. They get one answer, ten million times. Various analyses have observed that under stressed market conditions, leading AI models produce investment recommendations that are highly correlated, with some studies measuring correlations above 95 percent.

The second layer is psychological. For fifteen years, every dip in the U.S. equity market has been shallow, short, and rewarded. The COVID crash of 2020 was 34 percent in 33 days. Fastest bear market in modern history. Recovered in five months, the fastest bear-market recovery in 150 years. The 2022 drawdown recovered in 18 months. The April 2025 tariff selloff recovered in five weeks. If you started investing in your twenties after 2009, this is the only market you have ever known.

Retail has internalized the lesson. On April 3, 2025, the day after the first round of tariffs sent the market down 5 percent, individual investors bought a record $4.7 billion of stocks in a single day. In the first half of 2025 alone, individual investors added $1.55 trillion to U.S. markets. Where did the money go? Into the same cap-weighted ETFs that absorb the 401(k) flow. Vanguard ETFs alone took 37 percent of all U.S. ETF inflows. VOO alone took 16 percent.

People aren’t refusing to sell. They’ve just stopped choosing.

What could finally break this?

I won’t pretend I know. But there are four candidates worth thinking about, and the people under forty reading this, who have never lived through a real bear market, should pay particular attention.

1. The AI buildout disappoints. The biggest companies in the index, the same ones that absorbed the multiplier on the way up, are spending unprecedented sums on AI infrastructure. Hundreds of billions on data centers, chips, and electricity. The bet is that AI will eventually produce enough revenue to justify all this spending. So far, it hasn’t. Nvidia’s customer base is concentrated in a few cloud companies, and those cloud companies are spending faster than their AI products are bringing in money. If two or three quarterly earnings calls in a row produce the message “we are pulling back on AI capex,” the multiplier reverses. The same names that absorbed the inflow take the outflow. And remember the Nvidia dividend hike. When a company hands $80 billion back to shareholders, it has effectively conceded it cannot put that capital to better use itself. Not what you would expect at the peak of an investment cycle. More what you would expect when a company starts to wonder if the peak is behind it.

2. A dip that just doesn’t end. The dip-buying reflex isn’t built on macro analysis. It’s built on a fifteen-year track record where the strategy worked. It breaks when the data stops confirming it, not necessarily through a deeper dip, but through a longer one. Imagine a 30 to 40 percent decline that takes two years to bottom and then grinds sideways for another four years without a clean recovery. That experience converts dip-buyers into sellers because the strategy stops paying off in any window short enough for human patience. The cause doesn’t have to be exotic. Persistent inflation, a debt crisis, sustained earnings disappointment. Any of them can produce it. The common feature is duration, not depth. Think 1973 to 1982, not 2020.

3. A real recession with sustained job losses. The first three catalysts stress prices. This one stresses the actual flow of money into the market. The 401(k) bid requires Americans to have paychecks. 2020 doesn’t count as a real test, because government transfers replaced lost wages within weeks and contributions kept flowing. The version that actually tests the system is a recession with long, sticky unemployment. The candidate most discussed right now is AI-driven white-collar displacement. Junior consultants, paralegals, mid-level analysts, customer service. If aggregate 401(k) contributions actually fall for an extended period because there are fewer paychecks to draw from, the mechanism doesn’t reverse, but it slows. And the support everyone has been counting on starts to thin.

4. Bonds and stocks fall together for a sustained period. The most underappreciated catalyst. Target-date funds work because of an old assumption: when stocks fall, bonds rise. The TDF rebalancing rule depends on that. In 2022, that assumption broke for the first time in modern memory. Stocks fell, bonds fell, and the classic 60/40 portfolio had its worst year on record. That was the warning shot. If it happens again, longer and harder, the TDF rebalancing engine, the most predictable mechanical buyer in the market, starts to malfunction. Plan sponsors get nervous. Fiduciary lawsuits get filed. The most automatic part of the entire system starts to wobble. Almost no one is positioned for this.

I won’t pretend to know when this reverses. Anyone who tells you they do is selling something. But the job of someone who understands what has been built isn’t to predict the timing. It’s to make sure you know what you own.

If you have a 401(k), find out what’s actually in your target-date fund. Look at the top ten holdings. You’ll almost certainly find that you own more of seven companies than you realized. If you tell yourself you’re diversified because you own an “S&P 500 fund,” check the math. You’re diversified by ticker count, not by risk.

The market will keep doing what it does. The mechanism will keep running until it stops. Your job isn’t to predict when. Your job is to know what you own, and to make sure that the exposure you have, once you actually see it numerically, matches the exposure you thought you were buying.

In most cases, it won’t.

Chad

Chad Butler is the Founder and Chief Investment Officer of Harvest Lane Investment Partners LLC, a fee-only investment advisory firm registered with the State of Utah (CRD# 340042). This content is for educational and informational purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any security. Market statistics, historical data, and academic research referenced in this piece are drawn from publicly available sources including the Investment Company Institute (ICI Investment Company Fact Book and monthly statistical releases), S&P Dow Jones Indices methodology documents and public consultations, the Federal Reserve, public SEC filings, peer-reviewed academic research (including work by Xavier Gabaix and Ralph Koijen), and reporting from Reuters, Bloomberg, the Wall Street Journal, and CNBC. Historical market data and statistics are referenced for illustrative purposes only and do not predict future market behavior. Views expressed are those of the author as of the date of publication and are subject to change without notice. Statements regarding future events, including pending IPOs, proposed regulatory or index methodology changes, and potential market outcomes, are based on publicly available information at the time of writing and are subject to change. Past performance is not indicative of future results. Investing involves risk, including the potential loss of principal. Readers should consult with a qualified financial professional before making investment decisions. Additional information about Harvest Lane Investment Partners LLC is available in Form ADV Part 2A, available upon request or at adviserinfo.sec.gov.